On August 10, 2012, the President signed into law the Iran Threat Reduction and Syria Human Rights Act of 2012, Public Law 112-158 (“TRA”). Section 504 of the TRA amends section 1245(d)(4)(D) of the National Defense Authorization Act for Fiscal Year 2012, Public Law 112-81 (“NDAA”), which the President signed into law on December 31, 2011. The section 504 amendments to the NDAA take effect February 6, 2013. Regulations that revise the Iranian Financial Sanctions Regulations, 31 CFR Part 561 (“IFSR”), to implement section 504 of the TRA and Executive Order (“E.O.”) 13622 will be issued shortly.

254. What does section 504 of the TRA do?

Pursuant to the restrictions already in place under the NDAA, foreign financial institutions (“FFIs”) face restrictions on, or loss of, correspondent and payable-through account access in the United States if they knowingly engage in significant financial transactions with the Central Bank of Iran (“CBI”) or a designated Iranian financial institution, unless an NDAA exception, such as the significant reduction exception, applies. The NDAA significant reduction exception applies if the Secretary of State, in consultation with the Secretary of the Treasury and other agencies, has determined that the country with primary jurisdiction over the FFI has significantly reduced its purchases of Iranian crude oil during a specified period of time.

Effective February 6, 2013, section 504 amends the NDAA in several ways. Most importantly, it narrows the NDAA’s significant reduction exception to (a) exempt from sanctions only transactions that conduct or facilitate bilateral trade in goods or services between the country granted the exception and Iran, and (b) require that funds owed to Iran as a result of the bilateral trade be credited to an account located in the country granted the exception and not be repatriated to Iran. In addition, it -

(i) eliminates the distinction between state-owned or -controlled FFIs (not including foreign central banks) and private FFIs, thereby expanding the scope of sanctionable transactions for state-owned or -controlled FFIs with the CBI or designated Iranian financial institutions; and

(ii) clarifies that countries that have reduced their Iranian crude oil purchases to zero may continue to receive the significant reduction exception.

The sale of agricultural commodities, food, medicine, or medical devices to Iran (the “Humanitarian Exception”) is not impacted by section 504 of the TRA.

The purchase or acquisition of petrochemicals from Iran remain sanctionable activities and are not subject to the significant reduction exception.

255. Do the section 504 modifications restrict any other dealings with Iran?

Yes, the section 504 modifications also narrow the scope of transactions excepted from certain sanctions available under E.O. 13622. Accordingly, FFIs in countries that are determined by the Secretary of State to have significantly reduced their purchases of Iranian crude oil pursuant to the NDAA, that knowingly conduct significant financial transactions with the National Iranian Oil Company (“NIOC”), the Naftiran Intertrade Company (“NICO”), or otherwise for the purchase of petroleum or petroleum products from Iran, are only eligible for the significant reduction exception if the FFIs adhere to the bilateral trade restrictions, credit the funds to an account in the country with primary jurisdiction over the FFI, and do not repatriate the funds to Iran.

Example 1: A FFI in a country which has received a significant reduction exception and with primary jurisdiction over the FFI may facilitate a transaction enabling an oil refinery in that country to purchase crude oil from Iran without having exposure to U.S. correspondent account sanctions, so long as the transaction meets section 504’s bilateral trade requirements, the funds are credited to an account in the FFI in the country with primary jurisdiction over the FFI, and the funds are not repatriated to Iran.

Example 2: If, however, a FFI in a country which has received a significant reduction exception facilitates a third country’s crude oil purchase – even a third country with a significant reduction exception – from Iran, the FFI would have exposure to sanctions because the transaction was not solely for the FFI host country’s purchase of crude oil from Iran.

256. What transactions are impacted by section 504 of the TRA?

Starting February 6, 2013, significant financial transactions* knowingly conducted or facilitated by a FFI –

(i) with the CBI or designated Iranian financial institutions;

(ii) with NIOC or NICO (irrespective of the FFI involved); or

(iii) for the purchase or acquisition of petroleum or petroleum products from Iran (irrespective of the FFI involved);

may be subject to NDAA and/or E.O. 13622 sanctions unless –

(i) the country that has primary jurisdiction over the FFI conducting or facilitating such significant financial transactions has received a significant reduction exception; and

(ii) the significant financial transaction is for bilateral trade only, and any funds owed to Iran as a result of such trade are credited to an account at the FFI in the country that has primary jurisdiction over the FFI and are not repatriated to Iran.

Any FFI that knowingly facilitates significant transactions or provides significant financial services for Iranian-linked individuals or entities designated for activities related to terrorism or the proliferation of weapons of mass destruction pursuant to E.O.s 13224 and 13382 can be sanctioned under section 104(c) of the Comprehensive Iran Sanctions, Accountability, and Divestment Act of 2010 (“CISADA”) and section 561.201 of the IFSR even if those transactions are not sanctionable under section 1245(d) of the NDAA and section 561.203 of the IFSR.

*These do not include sales relating to the Humanitarian Exception.

257. To which jurisdictions does the significant reduction exception apply?

As of February 6, 2013, 20 jurisdictions have been granted a 180-day significant reduction exception.

The following jurisdictions received their 180-day significant reduction exception to NDAA sanctions on September 14, 2012: Belgium, the Czech Republic, France, Germany, Greece, Italy, Japan, the Netherlands, Poland, Spain, and the United Kingdom.

The following jurisdictions received their 180-day significant reduction exception to NDAA sanctions on December 7, 2012: China, India, Malaysia, Republic of Korea, Singapore, South Africa, Sri Lanka, Taiwan, and Turkey.

258. What is meant by section 504’s requirement that bilateral trade consist of trade in goods and services between the country with primary jurisdiction over the FFI and Iran?

OFAC interprets bilateral trade between Iran and the country with primary jurisdiction over the FFI to mean trade in only those goods or services originating in (e.g., produced in or substantially transformed in) –

(i) the country with primary jurisdiction over the FFI conducting or facilitating the transaction, or

(ii) Iran (for purposes of the import of Iranian-origin goods or services by the country with primary jurisdiction over the FFI),

and the trade in services cannot include brokering transactions involving goods or services from or to third countries.

Furthermore, the goods or services must be exported and sold directly to either the country with primary jurisdiction over the FFI (in the case of Iranian-origin goods or services), or Iran (in the case of goods or services originating in the country with primary jurisdiction over the FFI).

The Humanitarian Exception is not impacted by section 504’s bilateral trade limitations (see FAQ 265).

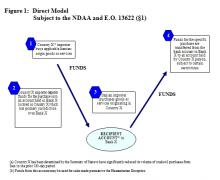

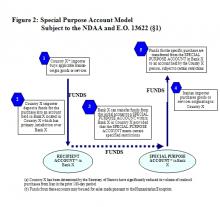

259. What can a FFI do with the funds resulting from the import of Iranian-origin goods or services once the funds are credited to an account? Can funds be transferred to other accounts?

Section 504 of the TRA requires that, in order for a sanctionable transaction to fall within the bounds of the significant reduction exception, any funds owed to Iran as a result of the bilateral trade transaction must be credited to an “account located in the country with primary jurisdiction over the [FFI].” For purposes of implementing this requirement, OFAC interprets the “account located in the country with primary jurisdiction over the [FFI]” to be an account in the country with primary jurisdiction over the FFI, and at the same FFI that facilitated the transaction for the importation of goods or services from Iran.

Once the funds are deposited in the FFI, they can be -

(i) used to pay for a purchase by Iran of goods or services originating in the country with primary jurisdiction over the FFI which are exported and sold directly to Iran, or for the Humanitarian Exception (see Figure 1); or

(ii) transferred to a SPECIAL PURPOSE ACCOUNT (see FAQ 260) within that same FFI, in the country with primary jurisdiction over the FFI, where the funds may be later debited to purchase goods or services originating in the country with primary jurisdiction over the FFI which are exported and sold directly to Iran, or for the Humanitarian Exception (see Figure 2).

The funds may not be repatriated to Iran.

260. What is a SPECIAL PURPOSE ACCOUNT for purposes of the NDAA’s significant reduction exception?

A SPECIAL PURPOSE ACCOUNT is an account set up with conditions and safeguards that require the account to be used only for bilateral trade in goods or services between Iran and the country with primary jurisdiction over the FFI, and for sales made under the Humanitarian Exception (see FAQ 265). Funds paid as a result of bilateral trade under the NDAA’s significant reduction exception may be transferred to a SPECIAL PURPOSE ACCOUNT, so long as the account is at the same FFI that facilitated or conducted the original transaction, in the country with primary jurisdiction over the FFI.

261. Are there any circumstances in which funds can be transferred to third-country financial institutions?

Transfers on or after February 6, 2013, of funds deposited in the RECIPIENT ACCOUNT or the SPECIAL PURPOSE ACCOUNT to third-country financial institutions are not covered by the NDAA’s significant reduction exception, and create exposure to sanctions for FFIs conducting or facilitating such transfers, unless the transfer is to pay a third-country exporter for sales made pursuant to the Humanitarian Exception (see FAQ 265).

262. Can funds be withdrawn from the RECIPIENT ACCOUNT or a SPECIAL PURPOSE ACCOUNT?

In order for the NDAA’s significant reduction exception to apply on or after February 6, 2013, funds withdrawn from the RECIPIENT ACCOUNT or SPECIAL PURPOSE ACCOUNT at the FFI may only be used to pay for bilateral trade or purchases relating to the Humanitarian Exception. Cash withdrawals from the RECIPIENT ACCOUNT or SPECIAL PURPOSE ACCOUNT would be deemed to fall outside of the scope of bilateral trade and would expose the FFI to sanctions. Bank checks written on the account may be used only to pay for bilateral trade or purchases relating to the Humanitarian Exception, and are subject to further restrictions set out in FAQ 263 below.

263. Who can receive payments from funds credited to a RECIPIENT ACCOUNT or SPECIAL PURPOSE ACCOUNT?

In order for the NDAA’s significant reduction exception to apply on or after February 6, 2013, the person receiving payment (e.g., the manufacturer or service provider) for goods or services being exported to Iran must be –

(i) a citizen, national, or permanent resident of the country with primary jurisdiction over the FFI maintaining the accounts containing the bilateral trade funds; or

(ii) an entity organized under the laws of the country with primary jurisdiction over the FFI maintaining such accounts.

Furthermore, the person receiving such payment may not be -

(i) the Government of Iran (as defined in 31 CFR Part 561.321) (“GOI”);* or

(ii) a financial institution that appears on the List of Foreign Financial Institutions Subject to Part 561, which is maintained on the Office of Foreign Assets Control’s Web site (www.treasury.gov/ofac).

*The term “Government of Iran” as defined in 31 CFR Part 561.321 includes: (a) The state and the Government of Iran, as well as any political subdivision, agency, or instrumentality thereof; (b) Any entity owned or controlled directly or indirectly by the foregoing; (c) Any person to the extent that such person is, or has been, or to the extent that there is reasonable cause to believe that such person is, or has been, acting or purporting to act directly or indirectly on behalf of any of the foregoing; and (d) Any person or entity identified by the Secretary of the Treasury to be the Government of Iran under 31 CFR Part 560.

264. Can funds be remitted to Iran or the GOI without exposure to sanctions?

No. If funds from the RECIPIENT ACCOUNT or the SPECIAL PURPOSE ACCOUNT are remitted, directly or indirectly, to Iran, or paid to any person that is the GOI, the FFI would be exposed to sanctions.

265. Can the funds be used for sales made under the Humanitarian Exception?

The NDAA generally exempts from sanctions sales made under the Humanitarian Exception (i.e., the sale of agricultural commodities, food, medicine, or medical devices from third countries to Iran). Funds deposited in the RECIPIENT ACCOUNT or the SPECIAL PURPOSE ACCOUNT can be used to pay for sales made pursuant to the Humanitarian Exception.

266. Does the November 8, 2012 designation of NIOC under E.O. 13382 impact the scope of permissible transactions by FFIs in significantly reducing countries?

Yes. On September 24, 2012, NIOC was identified as an agent or affiliate of Iran’s Islamic Revolutionary Guard Corps (“IRGC”) under section 312 of the TRA, and designated on November 8, 2012, under E.O. 13382 for providing services and support to the IRGC. Accordingly, CISADA applies to transactions with NIOC. As a result of these additional sanctions against NIOC, only transactions solely for the purchase of petroleum or petroleum products from NIOC will fall within the scope of the significant reduction exception. A FFI in a significantly reducing country that is found to knowingly conduct or facilitate other types of significant transactions with NIOC (i.e., transactions unrelated to the purchase of petroleum or petroleum products from Iran) would face exposure to CISADA sanctions.

Example 3: If a FFI in a country with a significant reduction exception facilitates a transaction enabling a company in that country to purchase drilling equipment from NIOC, the FFI risks restrictions on, or loss of, correspondent and payable-through account access in the United States, because the transaction was not solely for the purchase of petroleum or petroleum products from Iran.

267. What are definitions for the following NDAA terms: “significant financial transaction,” “knowingly,” “food, medicine, and medical devices,” “foreign financial institution,” and “country with primary jurisdiction over the FFI,”?

These definitions are set out in 31 CFR Part 561.